Differential Sum Explained

What’s A Differential Sum? (Not Dim Sum)

Category: Step 3: Sign Important Stuff | Tags: Banks, Finance, Loans, The Journey

To be honest, these two things have nothing in common, I was thinking of a catchy headline and the only thing that popped in my head was dim sum. Probably because I was hungry at the time I was writing this. But let’s concentrate!

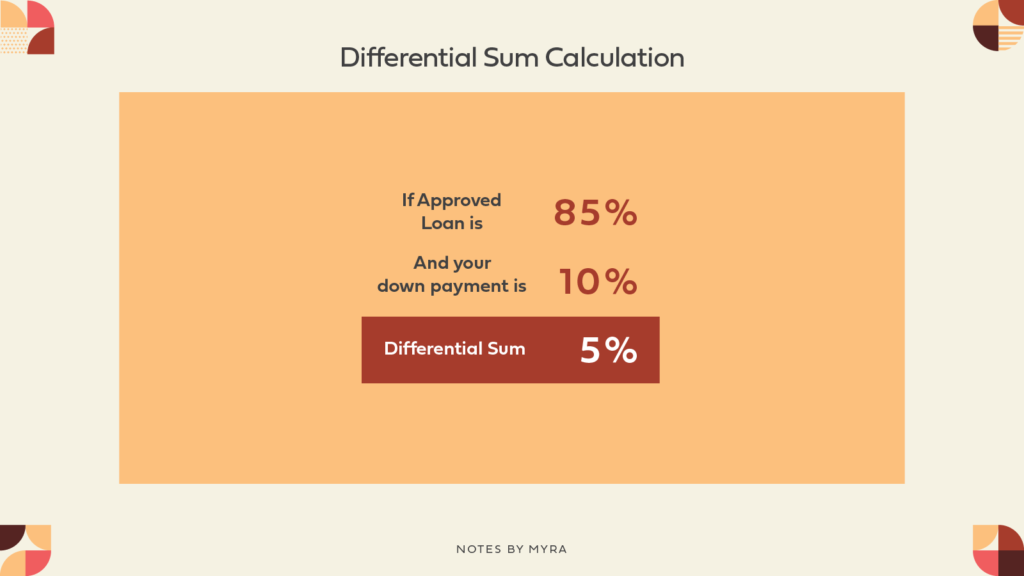

SO, a differential sum is payable upon the signing of agreement and is the difference between your property price, and loan amount (including the 10% down payment which normally, has already been covered ;D ). The full sum has to be paid to your property developer before you sign your loan agreement. Take a look at the illustration below to see how it’s calculated!

If your approved loan is 90%, and your down payment is 10%, no differential sum needs to be paid. Yay! But the loan approved is only 85% then you’d have to pay the balance of 5% to the developer before you can proceed.

Okay, so let’s get down to business. There are two common ways that you can pay for it:

Option 1:

You will need to bank transfer the balance to the developer’s account and send them the receipt for proof of payment.

Option 2:

You can withdraw the amount from your Account 2 in EPF at your nearest EPF center. It’s a simple application process that usually takes 3 to 7 days but do remember to bring a copy of your SPA and housing offer letter.

And that’s about it for this blog post! But if you need more information, don’t hesitate to drop a text!